How can you afford to live there? - Lower Healthcare costs

We live in another country for less than it would be to just pay for our health insurance in the United States.

I know a lot of Americans talk about healthcare in other countries a lot, but it really makes a difference for us. There are definitely some issues and there

We didn’t move to France for the healthcare, but it’s nice that it doesn’t feel like a slow-motion financial panic.

In the past year, I’ve cracked a tooth, twisted an ankle, and had not one but two surprise eye surgeries. It was a further surprise discovery that I was to remain conscious during the eye surgeries, so now that’s a thing I have done.

Any one of those surprises in New York would’ve required a spreadsheet and a stiff drink.

Occasionally useful information, always in your inbox.

France’s system is not perfect, but there does seem to be a better logic to it. It’s cheaper because it is managed centrally. While this is good overall at keeping costs down, it can also be impersonal, tough to schedule, and for a few things, feel almost impossible to get done.

Yet I sometimes had the same experiences in the US and the cost can much more expensive - normally at least 5 times as expensive, depending, in multipliers of some pretty bug numbers.

French healthcare is not free

There’s something very valid in the French frustration: most locals have been paying into this health system since their first job, while we’ve only recently chipped in.

On average, employees contribute 20–23 % of their salary into social charges (including healthcare) , and employers around 45 %—a huge fund built over decades (International Living has a fine writeup here).

In 2023, total contributions hit €142 billion for ~38 million beneficiaries—roughly €3,700 per person per year. Over 40 years, that’s nearly €150 000 each.

We, by comparison, have only been adding for a few years.

So yes—we should be aware of that difference.

We do pay now, but our lifetime tally is a fraction of that built-in equity.

Feeling a bit grateful seems like the least we can do.

Panic-free Healthcare

There’s lower stress, not just lower costs, with French healthcare

To be fair, a lot of my healthcare concerns have been kind of run of the mill and the French system has handled them nicely. If I had something more extreme or less common, I can’t say.

I accidentally cracked a tooth in France last year, which was a surprise cost. If that happened in New York, I’d have to reconsider my mortgage.

Supporting my work probably costs a lot less than your medical insurance!

I still don’t understand US healthcare

The US actually spends a lot of money on healthcare, but they don’t get much for it. There are reasons, of course, and a tendency to fall into all-or-nothing thinking, but shifts and improvements can be made. We can still fund research and have people paying less for insurance. We can.

France has limited choices to make: public, private, with a supplemental or not. Get the supplemental.

U.S. health insurance language is confusing: HMOs require referrals and stay in-network; PPOs offer more flexibility but cost more.

EPOs are stricter PPOs with no out-of-network coverage, and POS plans combine the worst of both worlds—referrals and some choice, if limited. High-deductible plans are cheap upfront but expensive if you have to use them. Then there’s Medicare for those over 65, Medicaid for low-income folks (state-dependent), and ACA Marketplace plans - ACA is Obamacare, to most people, but I still found it seriously confusing.

Quit your job? You get COBRA, where you pay full price, while also paying an extreme premium (an extremium?). Most people who insurance, get coverage through work, which is crazy enough. Even then, understanding what you actually have is another matter.

Some French people have asked me to explain it. I’ve tried. They laugh at the idea of a $10,000 bill, but it doesn’t really register that you could potentially get a few of those in a year. Neither does the part where the bill can change afterward, or that you’re supposed to argue with it, often without success.

I don’t think I really understood my healthcare plan in my entire adult life. I just felt lucky when something actually got covered.

I did ask about it. I did do a lot of research. I asked around.

When I was teaching, health insurance was something you could talk about at Happy Hours. It was topical. Once, a group of colleagues and created a Book Club for healthcare policies that met once a week.

Every year, we started the club again because we still needed it.

those conversations saved everyone thousands.

the approach is different

The French healthcare ecosystem is designed to treat care as a right, not a marketplace gamble. The system is tilted toward access, efficiency, and long-term public health rather than short-term profit.

Of course this has its problems as more doctors are needed, there are medical deserts in this country as well, it can be difficult to get appointments, and so on.

Almost everyone sees a general practitioner first. It’s baked into the system. You pick a médecin traitant, and if you don’t, you pay more.

That simple rule reins in unnecessary specialist visits and helps coordinate care. There’s a kind of quiet logic to it. You don’t get bounced around or sold on a menu of treatments—you get seen, usually quickly, by someone who knows your history.

There are problems with specialists, of course. When I was trying to see an audiologist for something, their office told me to “call back towards the end of the year” to see about an appointment.

I called them in March.

Still waiting…

Prices on display

Costs are known. That’s revolutionary compared to what I am used to.

Everything has a price—and the price is the price. The government negotiates it. You don’t walk into a lab for blood work and find out afterward that it cost $600 because someone billed it under a “hospital outpatient diagnostic panel” code. You pay €17.08. Or nothing, if your mutuelle picks it up.

A lot of the savings come from simply not doing weird expensive things.

Doctors also don’t graduate with crushing student loans. Hospitals aren’t privately held equity projects. There aren’t six different layers of billing departments pinning their tails on the donkey of your claim. Fewer middlemen, fewer faxes, fewer mystery charges.

And maybe most telling: the whole thing runs on a little green plastic card. The Carte Vitale. I slide it into a reader, it pulls up my national record, and voilà—my visit, reimbursed within days.

No chasing claims, no explaining to some insurer why I went to the doctor when I was sick. The bureaucracy isn’t fun, don’t get me wrong, but it’s rarely cruel.

Simpler and cheaper

People complain about it, but the French system is streamlined compared to the daunting American system, with oddly-named plans, deductibles, copayments, out-of-pocket minimums and maximums, pre-tax savings plans, etc. All of these additional “solutions” just seem to obscure the basic fact that healthcare in the US should all be easier and cheaper.

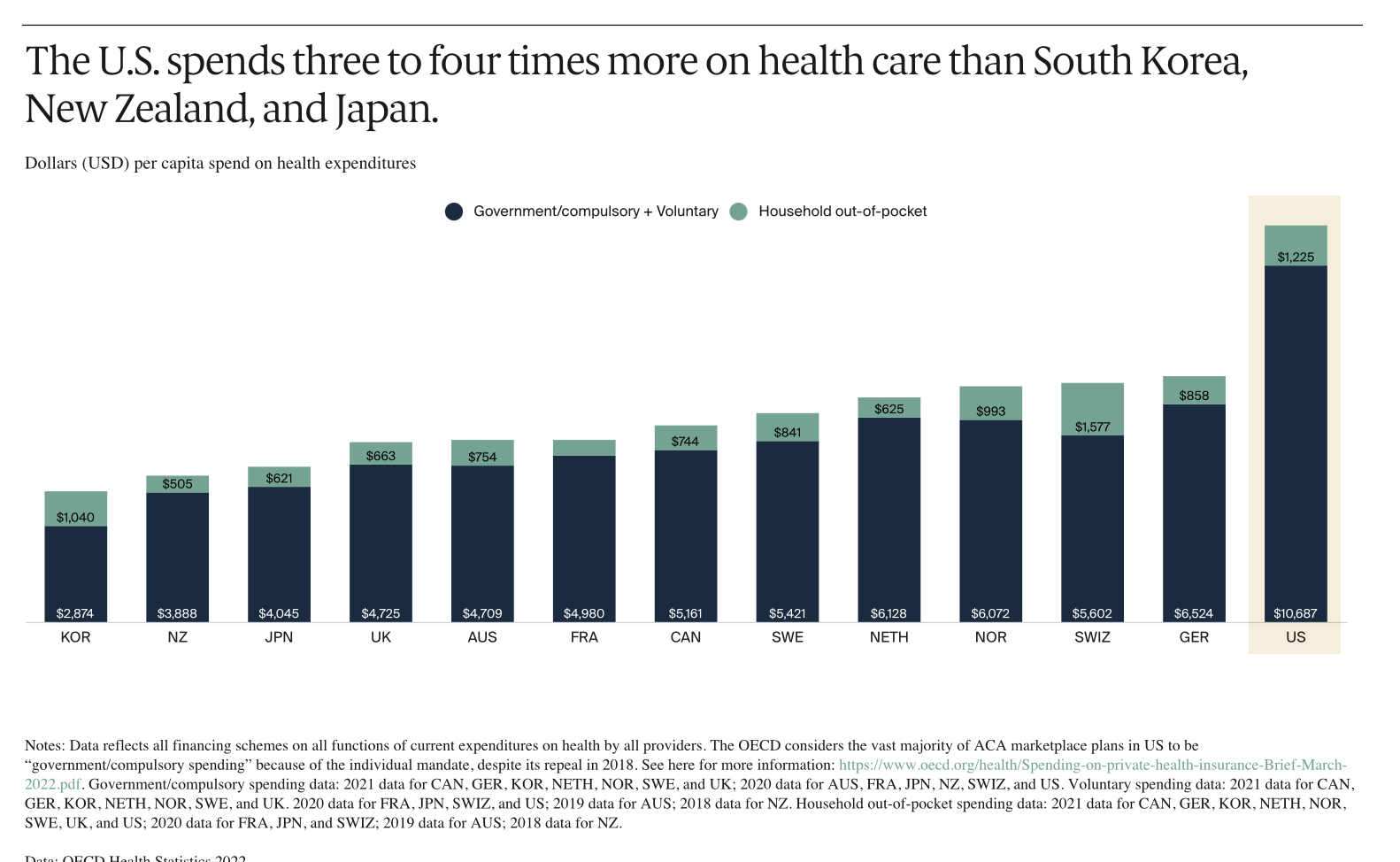

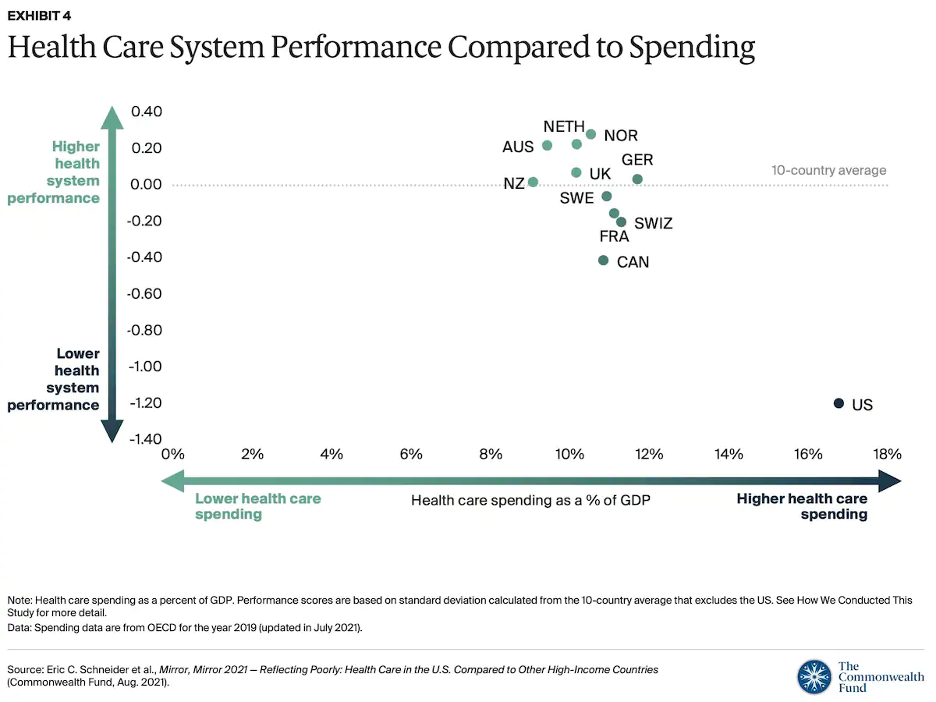

France’s system is one of the more expensive ones in the world, but still costs only 30% of the US system. The WHO ranked France #7 in the world in 2023, and the US at #18 in terms of quality of care.

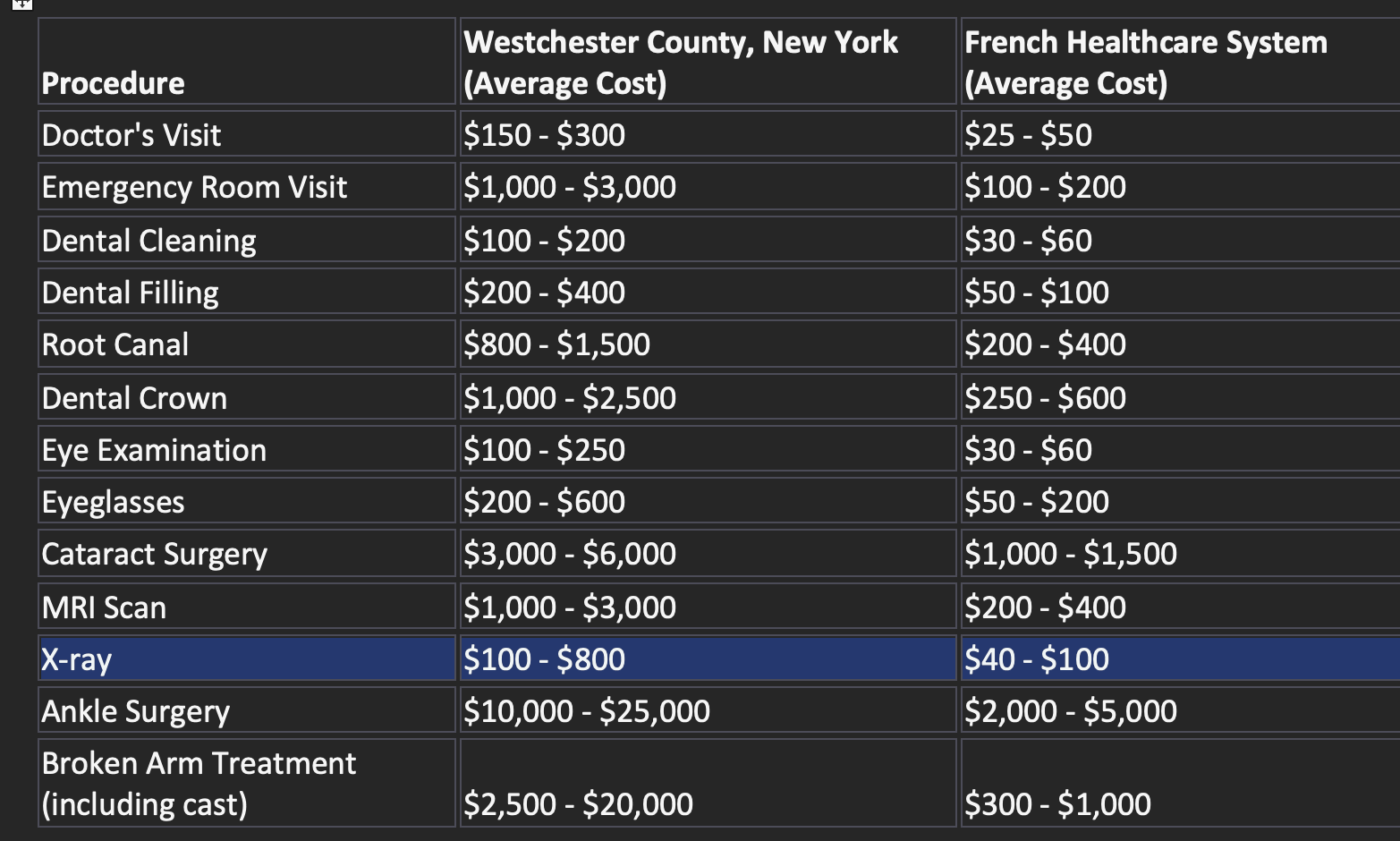

Here are some figures as an example. When I lived in New York City, my personal costs were on the higher end of these averages or over them. Always.